By Arun Menon

This report examines opex trends in the telecommunications network operator (TNO, or telco) market. This new edition has expanded the sample telco group coverage from 30 to 33 companies, and added a year of data coverage (2022). This new edition is now based on sample of telcos which more closely mirrors the globe. The regional splits for the sample telco group of 33 companies is spread across major regions with Asia representing 43.8% (of 2022 revenue total by HQ region), Americas 26.3%, Europe 20.3%, and MEA at 9.6%.

Telco revenues dropped by 5.9% on a YoY basis in 2022, to post $1,779.9 billion (B) – a record low in more than a decade. While the key factor behind the steep slump is AT&T’s April 2022 spinoff of its WarnerMedia unit, telcos have historically faced flat revenues with per year top-line growth in the range of 1-3% for several years, after adjusting for exchange rate fluctuations and COVID-19. To add to the woes, telcos have so far been unable to convert growth opportunities from 5G into major new revenue streams. As a result, telcos face the immense burden of keeping the profitability ticking amid stagnating revenues, high capex requirements, macro pressures, and fierce competition from new-age operators. While telcos have been able to deliver steady profitability margins amid flat to slight revenue growth environments for the past several years, they mostly resorted to traditional means of cutting costs in the past mitigation cycles, efforts which have been narrow and tactical in nature; for ex., asset sell-offs, real-estate rationalization, repair and maintenance outsourcing, shared services models. To drive sweeping cost efficiencies, telcos will have to implement dramatic, strategic measures to optimize their cost structure in order to increase and sustain profitability. Hence, understanding and effectively managing opex is crucial for telcos seeking success. Telco earnings reports make this obvious, as they highlight things like opex transformation programs, careful opex management, cost optimization initiatives, network efficiencies, and process automation.

Managing opex efficiently requires dissecting it further into standardized cost categories

Opex as a cost category is several times the size of capex and hence, provides ample opportunities for telco CxOs to reduce overall costs. The problem is that opex is a bit of a mystery due to complexities surrounding it – it’s hard to understand across companies, countries, and over time. Reporting categories, definitions, and accounting standards vary widely. This report solves the problem. We have created a taxonomy of opex categories, examined a broad cross-section of telcos, and calculated a detailed opex profile for both the individual companies and the overall telecommunications industry.

Key findings below:

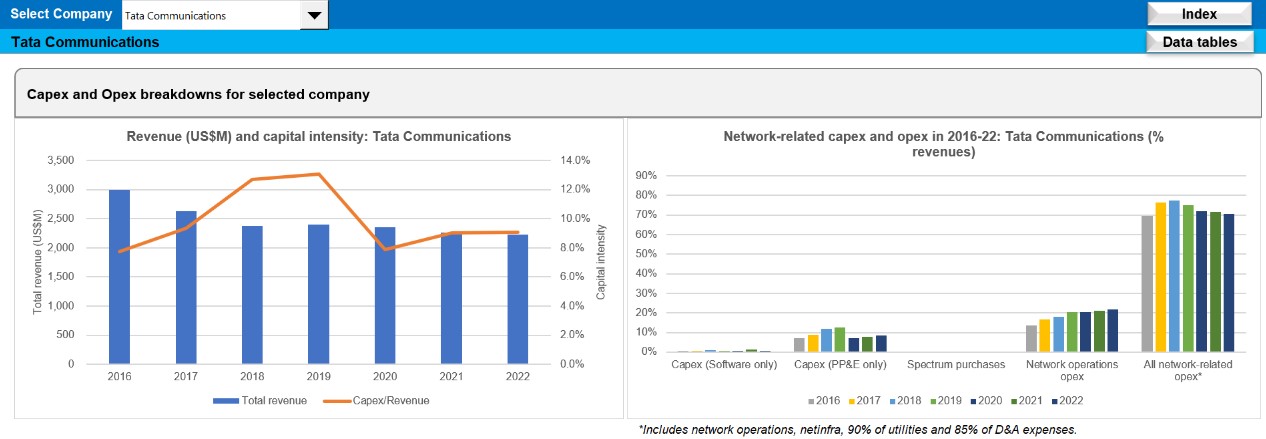

(1) For telcos, the network is their factory. The sum total of all network-related opex – including network operations (netops), netinfra (leasing, interconnection, and spectrum), utilities (90% assumed to be network-related), and depreciation (85%) – accounts for a staggering half (50.0%) of total opex, on average for 2016-22. The network-related portion of opex can vary by company though, for instance from the mid-30% range for Comcast and Charter Communications, to over 70% for PLDT and Airtel, and 80% of total opex for Tata Communications in India.

(2) Costs related to maintaining the network are one of the key opex elements for telcos. On average, network operations opex alone accounted for close to a fifth (17%) of total opex for telcos in the 2016-22 timeframe. This ratio has been rising over the years: network operations opex increased from 16.4% of total opex in 2016 to 17.5% in 2022. The upwards pressure is likely to continue. Further, network operations opex can vary noticeably across companies – 10 telcos spent over 20% of total opex on netops in our study, while at least one telco (Telkom Indonesia) spent over 30%.

(3) On the contrary, netinfra opex has been declining, particularly since 2019 due to implementation of a new accounting standard (IFRS 16) which caused telcos to stop recording most operating lease expenses within opex, as the underlying assets moved to the balance sheet. However, an increase in depreciation and amortization expenses has offset this decline.

(4) Utilities, content, and R&D opex average to 3.7%, 8%, and 0.8% of total opex, with lots of variation around these averages: Airtel spends about 11.4% of opex on utilities, content accounts for 32.7% of total opex for Comcast, and BT is a big spender on innovation with R&D accounting for 3% of total opex.

(5) Cost of devices, including both mobile and fixed CPE, averages to over 10% of total opex but surpasses 20% for some operators, mostly mobile-focused companies. Telcos have been clinging on to the strategy of subsidizing their customers’ purchase of new devices in exchange for long-term service contracts. While in the past this has helped prop up their revenue growth and customer base, it is now leading to higher customer acquisition costs.

(6) Sales & Marketing (including non-network customer support) and G&A averaged to 14% and 12.8% of total opex, respectively, for 2016-22. The sales & marketing category, though, exceeds 20% of total opex for a few telcos. SK Telecom, for instance, spent a whopping 40.5% of total opex on sales & marketing in 2022 – South Korea is especially witnessing cash-burning marketing campaigns by telcos to provide subsidies for mobile phone purchases (cost allocation done towards “sales and marketing” rather than “cost of devices” in this case). G&A costs was over 20% of total opex for at least five operators. One factor is the degree to which telcos rely on third-parties for core corporate functions, as well as the cost of insurance, HQ facilities, non-income taxes, and regulatory fees.

(7) Depreciation and amortization (D&A), while a non-cash expense, is the single largest opex category, amounting to an average of 22.6% of total opex across 2016-22 for the group of 33 telcos. This 22.5% is consistent with the global telco market, where D&A accounted for 21.5% of total opex in the same timeframe. D&A costs as a percent of opex for the group of 33 telcos grew from 21.6% in 2018 to 23.4% in 2022, due mainly to IFRS 16 implementation. At the operator level, D&A expenses vary widely. The more a telco owns and operates its own network assets and infrastructure, the higher are its D&A expenses.

(8) Labor costs are a significant contributor to a telcos’ total opex (>16%), and they stretch across multiple categories of spending: network operations, sales & marketing, and G&A. For the group of 33 telcos, labor costs per employee have been rising, which mirrors the global telco market trend. Labor costs per employee for the group of 33 rose from $47K in 2016 to $58.2K in 2022, vs. $47.7K in 2016 to $56.1K for the global telco market. Telcos are upskilling the existing workforce on digital platforms and other niche technologies, and hiring a new-generation of software savvy employees able to function in the telco of the future. The new-generation workforce of telcos will overlap with the talent pool targeted by ‘big-tech’ companies. The pool will include professionals with skill sets in network operations, software development, hardware, and IT infrastructure. As a result of this transition, the average telco employee salary is rising.

Implications

Many of the above results will not be surprising to those who track telcos closely. However, putting a credible number on a “gut feel” is a leap forward from the status quo. Vendors need to be able to position themselves effectively to customers. Telcos and analysts tracking them need to have an apples to apples comparison of how their costs compare to peers.

As far as public reporting goes, this study alone may not impact telcos’ opacity and inconsistency around opex. These practices have historic roots, in some cases, and old habits can be hard to break. But observers should recognize that the practices are often self-serving, and just because a company says an initiative saved money, doesn’t mean it really did. Company execs in every industry tend to dress up their financial results to look as attractive as possible, and telecom is no different.

___

*Companies included: Advanced Info Service (AIS), Airtel, Batelco, BT, Charter Communications, China Mobile, Chunghwa Telecom, Comcast, Du, Etisalat, Globe Telecom, KDDI, KPN, LG Uplus, Megafon, MTN Group, Oi, Ooredoo, Orange, PLDT, Proximus, Saudi Telecom (STC), Singtel, SK Telecom, Starhub, Swisscom, Tata Communications, Telecom Argentina, Telecom Italia, Telkom Indonesia, Telus, Turk Telekom, and Veon

- Table Of Contents

- Figure & Charts

- Coverage

- Visuals

Table Of Contents

- Abstract

- Results for Group of 33 Telcos

- Results by Company

- Taxonomy

- About

Figure & Charts

- Capex and Opex as % of Revenues – Group of 33

- Network-related capex and opex in 2016-22: Group of 33 (% revenues)

- Opex by category, 2016-22 average

- Network-related opex categories as % of total opex, 2016-22

- All network-related opex, % total

- Profit margins for group of 33 telcos, 2016-22 average

- Labor costs as a % of total opex

- Labor costs per employee (US$K)

- Opex items by company, % total opex: 2022

- Profitability margins by company, 2022

- Company-level revenue (US$M) and capital intensity

- Company-level network-related capex and opex in 2016-22

- Company-level opex by category, 2016-22 average

- Company-level network-related opex categories, as % of total opex, 2016-22

- Company-level all network-related opex as % of total opex

- Labor costs per employee (US$K): company vs. global telco average

- Labor costs as a % of total opex: company vs. global telco average

- Average profit margins, 2016-22: company vs. global telco average

- Company-level profitability trends, 2016-22

Coverage

Operator coverage:

| Advanced Info Service (AIS) |

| Airtel |

| Batelco |

| BT |

| Charter Communications |

| China Mobile |

| Chunghwa Telecom |

| Comcast |

| Du |

| Etisalat |

| Globe Telecom |

| KDDI |

| KPN |

| LG Uplus |

| Megafon |

| MTN Group |

| Oi |

| Ooredoo |

| Orange |

| PLDT |

| Proximus |

| Saudi Telecom (STC) |

| Singtel |

| SK Telecom |

| Starhub |

| Swisscom |

| Tata Communications |

| Telecom Argentina |

| Telecom Italia |

| Telkom Indonesia |

| Telus |

| Turk Telekom |

| Veon |

Visuals